Understand Qualifying Income Corporate Tax UAE. Crossfoot helps you optimize exemptions & stay compliant. Expert guidance you can trust.

Table of Contents

Qualifying Income Corporate Tax UAE: A Complete Guide for Free Zone Businesses

It was a typical Tuesday morning in Dubai when Ahmed, the founder of a thriving logistics company in JAFZA, called me with urgency in his voice.

*“I set up in a Free Zone for the 0% tax. Now everyone’s talking about Corporate Tax. Will I lose my zero-rate benefit?”*

Ahmed’s concern is one I hear daily. When the UAE introduced Federal Corporate Tax in June 2023, many Free Zone business owners felt the ground shift beneath their feet. The good news? The 0% rate isn’t gone—it has simply evolved.

This guide cuts through the confusion surrounding qualifying income corporate tax UAE. Whether you run a trading company, service provider, or holding entity, you’ll learn exactly how to qualify for—and maintain—the coveted 0% rate.

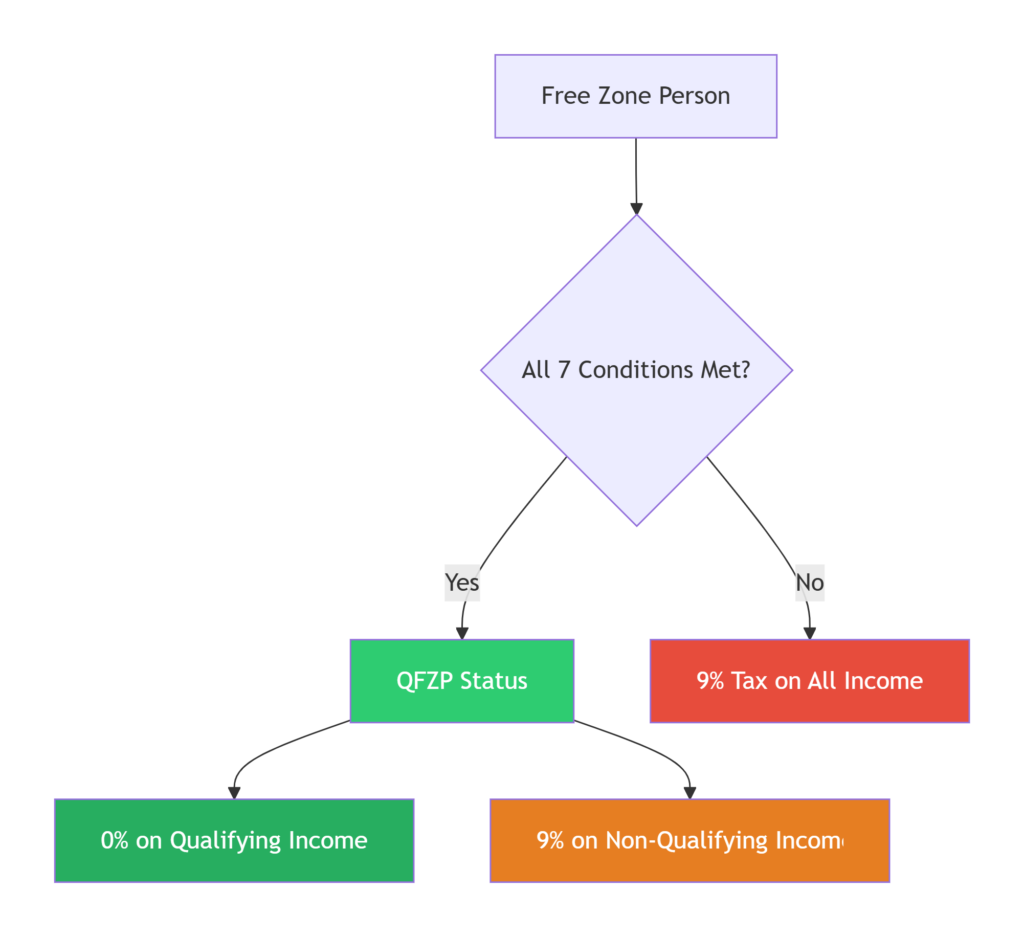

Understanding the Basics: What Is Qualifying Income Corporate Tax UAE?

Let’s start with clarity.

Under Federal Decree-Law No. 47 of 2022, the UAE introduced a federal Corporate Tax regime effective for financial years starting on or after June 1, 2023 . The standard rates are:

| Taxable Income | Applicable Rate |

|---|---|

| Up to AED 375,000 | 0% |

| Above AED 375,000 | 9% |

However, for Qualifying Free Zone Persons (QFZPs), a special regime applies. Their qualifying income is taxed at 0% —but only if they meet strict conditions. Any non-qualifying income is taxed at 9% .

This is the essence of qualifying income corporate tax UAE—a concept that determines whether your Free Zone business enjoys zero percent or pays the standard rate.

What Makes a Free Zone Business a “Qualifying Free Zone Person”?

Here’s where many get tripped up. Not every Free Zone company automatically qualifies for 0%. You must meet seven cumulative conditions :

The Seven Conditions for QFZP Status:

Incorporated or registered in a UAE Free Zone (including branches)

Maintains adequate substance in the Free Zone (physical presence, employees, operating expenditure)

Derives qualifying income from permitted activities

Has not elected to be subject to the standard 9% regime

Complies with transfer pricing rules and documentation requirements

Non-qualifying revenue does not exceed de minimis limits (5% or AED 5 million, whichever is lower)

Prepares audited financial statements in accordance with IFRS

Let me be direct: “Adequate substance” is non-negotiable. I’ve seen companies lose their QFZP status because they operated as mailbox entities with no real presence. The FTA expects to see:

- Physical office space in the Free Zone

- Qualified employees physically present

- Operating expenditures (payroll, rent, utilities)

- Core income-generating activities conducted within the Free Zone

Qualifying Income: The Heart of the Matter

Now, let’s tackle the core question: What exactly counts as qualifying income corporate tax UAE?

Under Cabinet Resolution No. 100 of 2023 and subsequent updates including Ministerial Decision No. 229 of 2025, qualifying income includes :

Qualifying Activities (Earn 0% Tax)

| Category | Examples |

|---|---|

| Manufacturing | Production of goods or materials |

| Processing | Treatment or refinement of materials |

| Trading of Qualifying Commodities | Metals, minerals, chemicals, energy, agricultural products (must have quoted price on recognized exchange) |

| Holding shares/securities | Passive investment holding |

| Ship operations | Ownership, management, operation |

| Reinsurance services | Risk transfer between insurers |

| Fund/wealth management | Investment advisory and management |

| Headquarter services | Management, strategy, admin to related parties |

| Treasury & financing | To related parties or for own account |

| Aircraft leasing | Financing and leasing of aircraft |

| Designated Zone distribution | Physical movement of goods through Designated Zones |

| Logistics services | Warehousing, transportation coordination |

| Ancillary activities | Closely related and necessary to main qualifying activity |

Excluded Activities (Generally Taxed at 9%)

- Transactions with natural persons (individual consumers)

- Banking activities (regulated)

- Insurance activities (excluding reinsurance)

- Finance and leasing to non-related parties

- Ownership or exploitation of immovable property (except commercial property in Free Zones transacting with other Free Zone persons)

The De Minimis Rule: Your Safety Net

Here’s a critical nuance that saves many businesses.

The de minimis rule allows a QFZP to earn some non-qualifying income without losing its 0% status—as long as :

Non-qualifying revenue ≤ 5% of total revenue OR AED 5 million (whichever is lower)

Example:

Your Free Zone trading company earns:

- AED 8,000,000 from qualifying activities

- AED 400,000 from a non-qualifying service

Total revenue: AED 8,400,000

Non-qualifying percentage: 400,000 ÷ 8,400,000 = 4.76%

You qualify! The non-qualifying portion is under 5% (and under AED 5 million).

But exceed either threshold, and you lose QFZP status for that tax year plus the following four years—meaning all income becomes taxable at 9% .

Domestic Permanent Establishment: A Hidden Trap

One of the most overlooked aspects of qualifying income corporate tax UAE is the concept of a Domestic Permanent Establishment (Domestic PE) .

If your Free Zone company has a place of business or presence outside the Free Zone in the UAE (like a mainland branch or warehouse), income attributable to that Domestic PE is automatically taxed at 9%.

However: Having a Domestic PE does not disqualify your QFZP status. Only the income tied to that mainland presence is taxed at 9%. The rest of your Free Zone income can still qualify for 0% .

Practical Compliance: What You Must Do

Based on my experience helping businesses navigate these rules, here’s your compliance checklist:

Monthly Monitoring

- Track qualifying vs. non-qualifying revenue to stay within de minimis limits

- Document all transactions with related parties

Annual Requirements

- Audited financial statements (IFRS)

- Corporate Tax return filing within 9 months of fiscal year-end

- Transfer pricing documentation for related-party transactions

- Substance verification (employee count, payroll records, lease agreements)

Registration Deadlines

- All Free Zone entities must register for Corporate Tax with the FTA

- Registration deadline: Within 3 months of incorporation or upon crossing revenue threshold

Common Mistakes That Cost Businesses Their 0% Status

I’ve seen too many companies lose their zero-rate benefit due to avoidable errors:

| Mistake | Consequence |

|---|---|

| Assuming all Free Zone income is automatically 0% | Unexpected 9% tax bill |

| No substance (virtual office only) | QFZP status denied |

| Exceeding de minimis by 1% | All income taxed at 9% for current + 4 years |

| No audited financial statements | Ineligible for 0% rate |

| Selling directly to mainland consumers | Income classified as non-qualifying |

A Real-World Scenario

Let me walk you through a typical client case.

Business: Dubai-based Free Zone trading company (commodities)

Annual revenue: AED 15,000,000

Breakdown: AED 14,000,000 commodity trading (qualifying) + AED 1,000,000 consulting to mainland client (non-qualifying)

Analysis:

- Non-qualifying revenue: AED 1,000,000

- Total revenue: AED 15,000,000

- Percentage: 6.67% → exceeds 5% threshold

- AED 1,000,000 also exceeds AED 5 million? No, but percentage fails.

Result: The company loses QFZP status. All AED 15,000,000 becomes taxable at 9%—a tax liability of AED 1,350,000 instead of just AED 90,000 on the non-qualifying portion.

Lesson: Monitor your revenue mix monthly. Consider structuring mainland consulting through a separate entity.

Recent Updates for 2025-2026

The regulatory landscape continues to evolve. Key updates include:

Ministerial Decision No. 229 of 2025 (retroactive to June 1, 2023):

- Expanded list of qualifying commodities (now includes environmental commodities)

- Tightened qualifying IP rules (income limited to R&D spend with 30% uplift cap)

- Clarified ancillary activities (must be directly linked to main qualifying activity)

De minimis rule unchanged at 5% or AED 5 million.

How Crossfoot Can Help

Navigating qualifying income corporate tax UAE requires specialized expertise. At Crossfoot, we help Free Zone businesses:

Assess your QFZP eligibility before filing

Track qualifying vs. non-qualifying revenue monthly

Prepare audited financial statements compliant with IFRS

File Corporate Tax returns accurately and on time

Document transfer pricing for related-party transactions

Substance verification to prove your Free Zone presence

With over 435+ businesses served and a 98% client satisfaction rate, we’ve guided countless Free Zone entities to maintain their 0% tax benefit.

Final Thoughts

The qualifying income corporate tax UAE framework isn’t designed to penalize genuine Free Zone businesses—it’s designed to reward those with real substance and compliant operations. The 0% rate remains available, but it requires intentional structuring, diligent monitoring, and professional support.

Don’t wait for an FTA audit to discover you’ve lost your QFZP status. Be proactive. Get clarity. Stay compliant.

Ready to Secure Your 0% Tax Rate?

Contact Crossfoot today for a Free Zone Tax Health Check.