Table of Contents

Navigating the Maze: Solving Cross-Border Banking Challenges in 2026

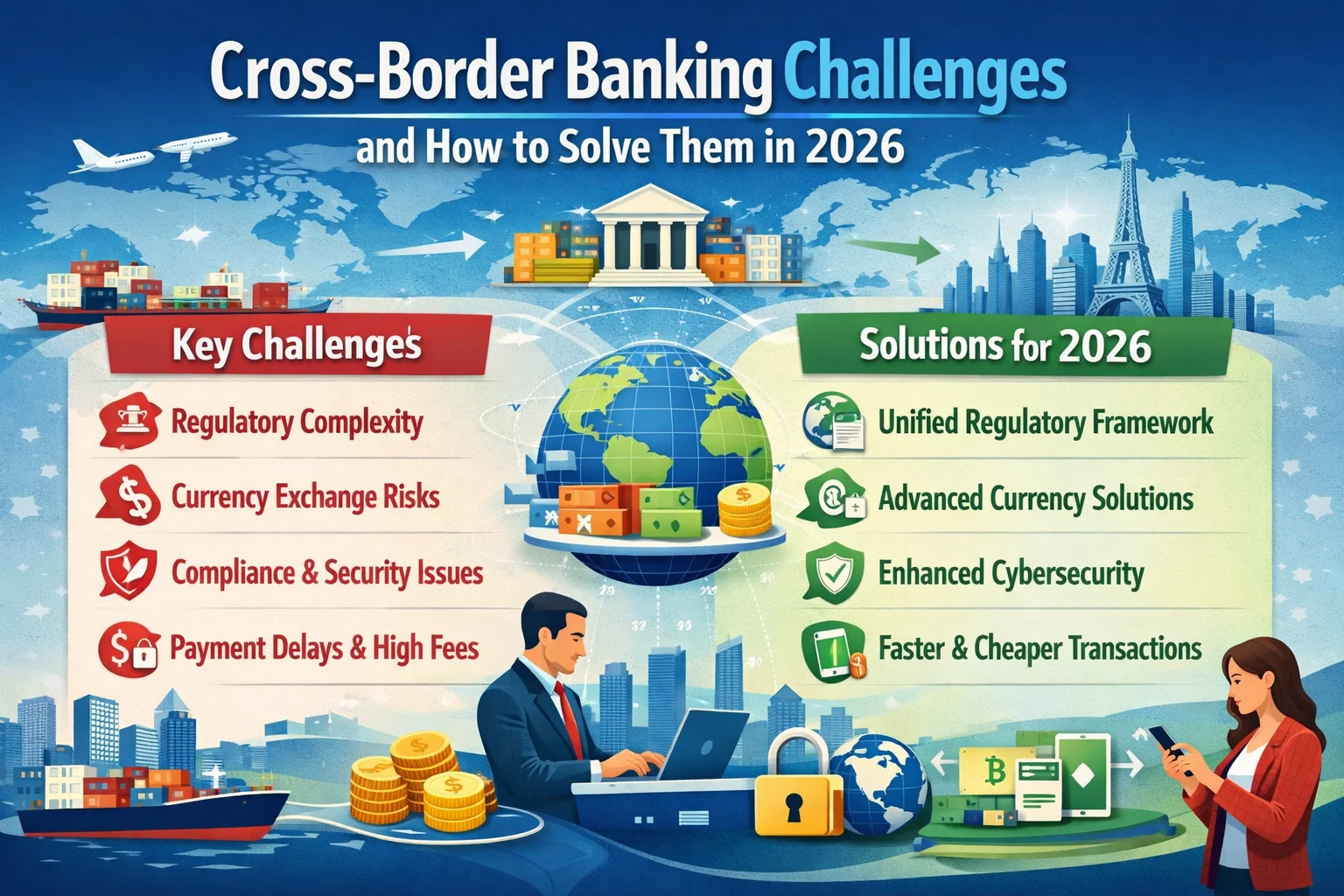

The Global Money Maze: Why Your Business Is Losing Time, Money, and Sleep

Picture this: You’re closing a major deal with a client in Germany. The product is perfect, the contract is signed, and everyone’s excited. Then comes the payment—a “simple” international transfer from Dubai to Berlin. Days pass. Then weeks. Your accounting team is fielding frantic emails while you’re stuck explaining to suppliers why their payments are delayed. The funds finally arrive, but with $2,800 mysteriously missing in fees and poor exchange rates.

This isn’t a rare horror story—it’s Tuesday for businesses operating across borders. Cross-border banking challenges cost companies billions annually in hidden fees, operational delays, and lost opportunities. As we approach 2026, these pain points are intensifying despite technological advances.

I’ve witnessed this firsthand through our work at Crossfoot. One client, a Dubai-based tech firm expanding to Singapore, discovered they were losing 4.3% of every international transaction to layered fees and currency spreads. Another, a manufacturing business with suppliers across three continents, had two full-time employees dedicated solely to tracking international payments and reconciling discrepancies.

The global payment market is projected to reach $2.5 trillion by 2025, yet the fundamental cross-border banking challenges remain stubbornly complex. But here’s the good news: 2026 brings unprecedented solutions if you know where to look.

The Hidden Cost Carousel: Understanding Today’s Cross-Border Realities

The Fee Maze That Eats Your Profits

Most businesses focus on the obvious—transfer fees. But the real killers are hidden in plain sight:

| Fee Type | Typical Cost | Why It Hurts |

|---|---|---|

| SWIFT/Intermediary Fees | $15-50 per hop | Unpredictable, multi-bank chain |

| Currency Spread Markup | 1.5-3% | Hidden in exchange rates |

| Receiving Bank Charges | 0.1-0.5% | Often unexpected upon arrival |

| Compliance Screening | Variable | Delays + potential rejection fees |

A Bank for International Settlements study reveals that sending $200 internationally still costs an average of 6.5%—barely improved from a decade ago. For businesses, this means eroded margins on every export and import transaction.

The Regulatory Patchwork Quilt

Every country has become a fortress of financial regulations since 2008’s global reforms. The European Union’s AMLD6 (6th Anti-Money Laundering Directive), GCC’s evolving compliance frameworks, and the U.S.’s OFAC requirements create a labyrinth where one missed checkbox can freeze funds for weeks.

One of our clients learned this painfully when a routine payment to a Malaysian vendor was flagged because “Technology Solutions Ltd.” matched a partial name on a sanctions list. The funds were held for 22 days during investigation—nearly collapsing a critical supply chain.

The Technology Disconnect

You use Slack for communication, Asana for project management, and QuickBooks for accounting. But for international payments? You’re back to fax-like systems. SWIFT, while reliable, operates on technology principles older than most of your employees.

The irony? We live in an age of instant everything, yet cross-border banking challenges include payment tracking systems that offer less visibility than a $20 food delivery app.

2026’s Game Changers: Solutions on the Horizon

The Rise of Real-Time Cross-Border Networks

2026 marks the tipping point for real-time cross-border systems. The Bank of England and Monetary Authority of Singapore’s successful linking of their real-time payment systems shows what’s possible. These bilateral corridors eliminate intermediaries, cutting settlement times from days to minutes.

For businesses, this means:

- Cash flow predictability restored

- Just-in-time inventory management

- Reduced working capital buffers

- Actual financial agility

Blockchain Goes Mainstream (Quietly)

Forget cryptocurrency volatility—the real blockchain revolution is happening in banking back-ends. J.P. Morgan’s JPM Coin system now handles $1 billion daily in corporate payments. What makes 2026 different? Interoperability between different blockchain systems.

Practical application: A Dubai exporter gets paid by a French buyer in euros, converted to AED instantly at near-mid-market rates, with full transaction transparency and immutable records for accounting. No guessing games, no hidden fees.

AI-Powered Compliance That Actually Helps

Current compliance is like airport security—everyone gets the same intrusive screening. 2026’s AI systems are shifting to “known traveler” models for trusted businesses.

Machine learning algorithms now analyze your company’s complete transaction history, creating a compliance profile that speeds legitimate payments while focusing scrutiny where it belongs. The result? 90% fewer false positives and clearance times measured in hours, not weeks.

The Corporate Multi-Currency Revolution

Forward-thinking banks are finally offering what businesses actually need: true multi-currency accounts with local account details in major markets. Receive USD with US routing numbers, EUR with IBANs, and GBP with sort codes—all from one dashboard.

This eliminates correspondent banking layers entirely. When your German client pays your “local” German account, it’s a domestic transfer. The funds then sweep into your central currency hub automatically.

The Human Element: What No Technology Can Replace

Building Financial Bridges, Not Just Transactions

During my years at Crossfoot, I’ve learned that solving cross-border banking challenges requires something beyond technology: relationship intelligence. We maintain what we call a “banking relationship map” for clients—knowing which bank managers in which countries actually answer their phones, who understands your industry, and which institutions move faster for established relationships.

This human network proved invaluable when a client needed emergency funds transferred from the UK to cover a Saudi Arabian payroll during an unexpected delay. Our direct contact at the receiving bank accelerated what would have been a 5-day process to 8 hours.

The Cultural Compass

Banking isn’t just about money—it’s about cultural understanding. A “urgent” payment request means different things in Japan versus Mexico. Formal documentation requirements vary dramatically between Switzerland and India.

We once saved a client from a critical error by recognizing that their “standard” payment authorization wouldn’t satisfy Korean banking regulations. The fix took 20 minutes of our time but saved 3 weeks of potential delay.

Your 2026 Action Plan: Practical Steps Starting Today

Phase 1: The 90-Day Diagnostic (Q1 2026)

- Map Your Money Flows

- Chart every international payment route

- Identify all fee layers (ask banks for complete breakdowns)

- Measure actual timing, not promised timing

- Benchmark Your Costs

- Compare rates across 3-4 providers

- Include hidden costs like account maintenance fees

- Calculate your true total cost of cross-border operations

- Compliance Health Check

- Review your KYB (Know Your Business) documentation

- Ensure beneficiary information is complete and updated

- Identify your highest-risk transaction patterns

Phase 2: The Solution Implementation (Q2-3 2026)

- Technology Stack Upgrade

- Pilot next-gen payment platforms (ask about API integration)

- Test blockchain-based solutions for high-volume corridors

- Implement multi-currency account structures

- Relationship Optimization

- Consolidate banking partners where possible

- Establish direct contacts at each institution

- Create escalation protocols for time-sensitive transactions

- Process Redesign

- Automate payment approvals based on rules

- Implement real-time tracking dashboards

- Train teams on new systems and compliance requirements

Phase 3: Continuous Optimization (Ongoing)

- Monthly Review Cycle

- Analyze fee trends and timing metrics

- Stay updated on regulatory changes in your markets

- Test emerging solutions on small transactions first

The Crossfoot Difference: Your Strategic Banking Partner

At Crossfoot, we’ve transformed from traditional accountants to financial navigation specialists. Why? Because we watched too many brilliant businesses struggle with cross-border banking challenges that had nothing to do with their core competencies and everything to do with financial system complexity.

Our approach combines:

- Technical mastery of emerging payment technologies

- Regulatory intelligence across the GCC and beyond

- Human relationships with financial institutions worldwide

- Process optimization that integrates with your operations

One client, a Dubai-based e-commerce company, reduced their international payment costs by 63% and improved settlement times from an average of 4.2 days to 6 hours after implementing our tailored cross-border strategy. More importantly, they reclaimed approximately 15 hours per week of accounting team time previously spent on payment tracking and reconciliation.

The Borderless Future: Not Just Possible, But Profitable

As we approach 2026, the landscape is shifting from mere problem-solving to strategic advantage creation. Businesses that master their cross-border financial operations gain:

- Cost leadership through optimized fee structures

- Competitive agility with faster settlement cycles

- Risk mitigation via robust compliance frameworks

- Strategic insight from consolidated global financial data

The most forward-thinking companies aren’t just solving cross-border banking challenges—they’re building financial infrastructure that becomes a competitive moat. They’re the ones who will acquire international competitors more easily, expand into new markets faster, and attract better financing terms.

The question isn’t whether you can afford to address these challenges in 2026. It’s whether you can afford not to.

Ready to transform your cross-border operations from a cost center to a competitive advantage? At Crossfoot, we combine financial expertise with technological insight to create tailored solutions for businesses navigating international markets. Explore our corporate accounting services or schedule a complimentary financial infrastructure review to prepare your business for 2026’s borderless opportunities.

Share your biggest cross-border banking pain point in the comments below—I’ll respond personally with specific insights for your situation.