Table of Contents

Debt & Equity Structuring: The Architect’s Guide to Building Business Resilience

Imagine standing at a crossroads.

To your left, a well-paved, clearly marked road—predictable, with a known toll. To your right, a less-defined path winding into beautiful, uncharted territory, offering a share of the treasure at journey’s end. Which do you choose? This isn’t a fable; it’s the fundamental decision every founder and CEO faces when funding their vision. This is the world of debt and equity structuring.

More than just financial jargon, your capital structure is the DNA of your company’s future. It dictates who has a say, how much risk you shoulder, and ultimately, what kind of business you’re building. Getting it right can propel sustainable growth. Getting it wrong can shackle potential.

As someone who’s guided numerous businesses through this complex terrain, I’ve seen the relief in an owner’s eyes when the puzzle pieces click—when debt and equity aren’t seen as adversaries, but as complementary tools in a master blueprint. Let’s draw that blueprint together.

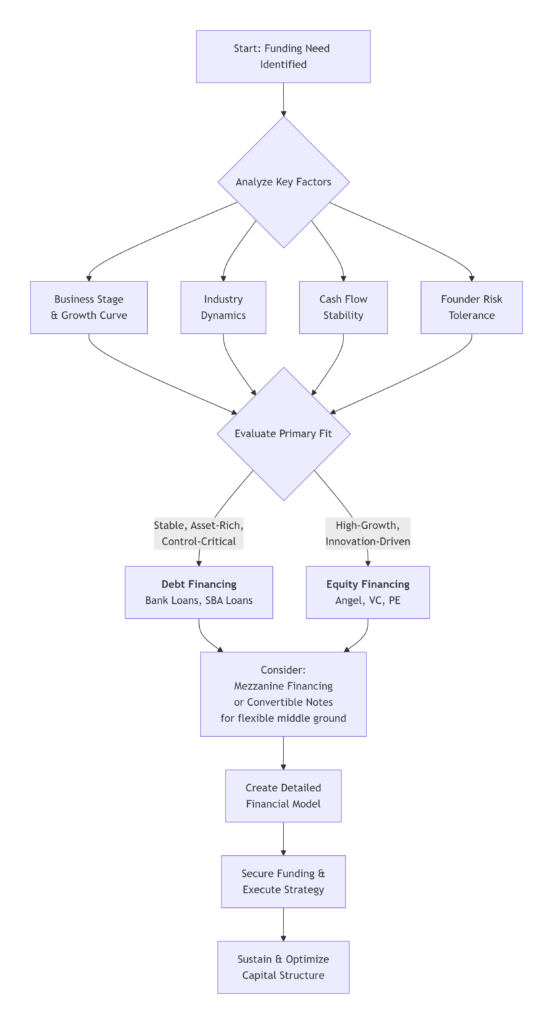

Debt vs. Equity: More Than Just Money

At its core, the choice is about control versus cost, obligation versus partnership.

Debt Financing is like taking on a disciplined landlord. You borrow a sum (the principal) and agree to repay it with interest over time. The lender, be it a bank or an institution, doesn’t care if your year is spectacular or miserable—they want their fixed payment. Your relationship is transactional. The upside? You keep full ownership and all future profits. The downside? The relentless monthly obligation, which can feel like a weight during lean months. Assets often act as collateral, turning business risk into personal risk.

Equity Financing, on the other hand, is inviting a committed partner into your home. You exchange a percentage of ownership (shares) for capital. This partner shares in your risks and rewards. If you fail, they lose their investment. If you soar, they reap a portion of the gains. This aligns long-term interests but dilutes your control. Major decisions may now require a board vote.

Here’s a quick comparison to crystallize the distinction:

| Feature | Debt Financing | Equity Financing |

|---|---|---|

| Nature | Loan to be repaid | Sale of ownership stake |

| Control | Retained by owner | Shared with investors |

| Cost | Fixed interest expense | Share of future profits |

| Risk | Fixed repayment obligation; collateral at risk | Dilution of ownership & control |

| Best For | Predictable cash flows, asset-heavy businesses, retaining control | High-growth startups, R&D, scaling rapidly |

The Strategic Mix: Finding Your Golden Ratio

The million-dollar question is never “debt OR equity?” but “debt AND equity in what proportion?” This is your capital structure. There’s no universal formula, but several key factors guide the decision:

1. Business Stage & Growth Trajectory

A nimble startup with explosive growth potential but no steady revenue is prime for equity (venture capital, angel investors). It needs fuel, not another bill. A mature manufacturing firm with stable cash flows and hard assets is a candidate for debt—using predictable earnings to leverage growth without giving up shares.

2. Industry Dynamics

Capital-intensive industries (real estate, manufacturing) often lean on debt secured against their tangible assets. Tech or service-based firms, whose main asset is intellectual property and people, traditionally attract equity.

3. Cash Flow Stability

This is the heartbeat of your debt capacity. Lenders scrutinize your cash flow statements. Consistent, predictable cash flow? You can service debt. Volatile, seasonal income? Equity or very conservative debt is safer.

4. Risk Tolerance & Founder Vision

This is the deeply personal element. How much sleeplessness can you handle? A debt-heavy structure adds financial risk. An equity-heavy structure dilutes your control. Your appetite for each defines your path.

Advanced Structuring: Beyond the Basics

The real art begins when you layer these tools creatively.

The Mezzanine Layer: Think of this as a hybrid. It might be subordinated debt (paid after senior loans) with an equity kicker (like warrants to buy shares later). It’s more expensive than senior debt but less dilutive than pure equity. It’s a fantastic tool for funding acquisitions or significant expansions.

Convertible Notes: A darling of the startup world, this begins as debt that automatically converts into equity during a future funding round at a discounted rate. It’s a way to delay valuation debates while providing early capital.

Seller Financing: In acquisitions, the seller acts as the bank, lending part of the purchase price to the buyer. This aligns interests for a smooth transition and demonstrates the seller’s confidence in the business’s future.

Common Pitfalls & How to Avoid Them

In my advisory role, I’ve helped clients untangle avoidable mistakes:

- The Debt Overhang: Taking on too much high-interest debt stifles cash flow. Rule of thumb: Your EBITDA should comfortably cover interest payments by at least 3x.

- Dilution Disillusionment: Giving away too much equity too early can leave founders with little reward after years of sweat. Always model future funding rounds to see where your ownership ends up.

- Ignoring Covenants: Bank loans come with strings—financial covenants (e.g., maintaining a minimum debt-to-equity ratio). Breaching these can force immediate repayment. Read the fine print!

- Misalignment with Investors: Not all money is equal. An investor seeking a 3x return in 5 years has a very different agenda than one building a legacy asset. Choose partners whose goals mirror yours.

A Framework for Decision-Making

When evaluating your options, walk through this checklist:

- Diagnose: What is the capital for (working capital, equipment, acquisition, R&D)?

- Quantify: How much do we truly need? Add a buffer, but avoid excess.

- Project: Create detailed, conservative cash flow forecasts under different scenarios.

- Explore: Talk to multiple banks, investors, and advisors. Terms vary wildly.

- Model: Map out the impact on ownership, control, and financials for 3-5 years.

- Align: Ensure the structure supports your strategic plan, not just fills an immediate hole.

The Human Element: It’s Your Story

Ultimately, debt and equity structuring is not a spreadsheet exercise. It’s a narrative about your ambition, your confidence, and your definition of success.

I recall advising a second-generation family business owner. He was risk-averse, leaning entirely on slow, organic growth funded by profits. His competitor took on strategic debt, modernized equipment, and captured market share. We worked on a moderate debt structure, secured against their property, to fund a crucial expansion. It wasn’t just about numbers; it was about helping him see that prudent leverage was a tool to secure his family’s legacy, not jeopardize it. Today, his business is thriving, and he sleeps just fine.

Visualizing Your Capital Structure Journey

Building Your Blueprint for Success

Your capital structure is a living, breathing part of your business. It should be revisited annually or when a major strategic shift occurs. The goal isn’t perfection on day one; it’s building a framework adaptable enough to support your evolving story.

The most successful leaders understand that debt and equity structuring is a strategic dialogue—a continuous process of balancing cost, control, and courage.

Ready to Architect Your Business’s Financial Future?

At Crossfoot, we move beyond basic bookkeeping to become strategic partners in your growth. We help you analyze your cash flow, model different debt and equity structuring scenarios, and build a capital plan that aligns with your ambitions—so you can make financial decisions with clarity and confidence.

Let’s build something resilient together.

📞 Schedule a Free Strategy Session with Our Financial Architects